ON THE KOLMOGOROV QUASIMARTINGALE PROPERTY

Abstract: Let  be a sequence of real-valued random variables (r.v.), which are centered,

square integrable and independent. A well-known result, due to Kolmogorov, states that

if

be a sequence of real-valued random variables (r.v.), which are centered,

square integrable and independent. A well-known result, due to Kolmogorov, states that

if

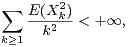

| (i) |

then  converges almost surely (a.s.) to 0, where

converges almost surely (a.s.) to 0, where

This paper is devoted to the interpretation of condition (i). For instance, it is shown that if

the r.v.  are weighted Rademacher r.v., then (i) is equivalent to the fact that

are weighted Rademacher r.v., then (i) is equivalent to the fact that

is a quasimartingale (

is a quasimartingale ( being the natural filtration associated with the

sequence

being the natural filtration associated with the

sequence  ).

).

The problem of the interpretation of (i) for Banach space valued r.v.  is also

studied.

is also

studied.

2000 AMS Mathematics Subject Classification: Primary: -; Secondary: -;

Key words and phrases: -